Explanatory Note: How the Sri Lankan Economy Crashed

Disclaimer:

- This is an explanatory note based on a lecture I did for my debate students last year. This is not an opinion piece and should not be republished/quoted. This is only for educational purposes.

- Views expressed are mine and mine alone and should not be attributed to my employer or any other institution with which I am affiliated

- I will try and get this translated into Sinhala and Tamil. If any translators can help out, please contact me

So… How did we get into this mess?

TLDR/SUMMARY

1. STRUCTURAL FACTORS

1.1 Unsustainable Accumulation of Debt

Since independence, every Sri Lankan government across the political spectrum has followed a debt-financed development strategy. This strategy can be justified as long as:

i) You spend the debt on projects that contribute significantly to the economy

ii) You don’t accumulate debts beyond what you can repay.

As a low-income country, Sri Lanka had access to concessionary debt at no interest or very low interest rates (often below 0.5%) from multilateral (e.g. World Bank, ADB) and bilateral lenders (e.g. UK for Victoria Dam, World Bank for Mahaweli Development Scheme, etc.). In 2009, however, Sri Lanka graduated to middle-income level and no longer had access to concessionary loans. Therefore, rather than getting loans at 0.05% interest, we now had to borrow from international capital markets (using tools like International Sovereign Bonds — ISBs) and bilateral lenders (e.g. loans from the China EXIM bank, currency swaps with India) at 5–7% interest (and at times even more).

Instead of recalibrating our economic policies to reflect this change in development finance, we continued with our debt-led growth strategy (now borrowing at 7% instead of 0.05%). To make matters worse, we spent a lot of that money on non-tradable infrastructure projects, which didn’t contribute anything significant back into the economy (i.e. not job creating, not export revenue generating). As a result our debt levels increased significantly with accumulated interest payments accounting for about 1/3 of our yearly debt repayments now.

I personally like to use the Debt to Government Revenue ratio to demonstrate how bad things are, because the Debt to GDP ratio doesn’t provide an accurate picture of how easily a country can pay back their loans. As shown in Figure 1, according to a paper in 2020, Sri Lanka’s Debt-GDP ratio is around 120%, but more than 70% of our government revenue goes towards servicing debt. This means that for every rupee of tax a Sri Lankan citizen pays, only 30 cents are used for national services — the remaining 70 cents are used to pay debt interest. Japan, for example, has a Debt-GDP ratio of 250%, but their interest payments are less than 10% of government revenue.

Following the conclusion of the war, Sri Lanka had an ideal opportunity to place its economy on a sustainable footing, by investing in improving our renewable energy sector (e.g. solar power, wind energy, etc), increase access to education and healthcare, integrating regions such as the North, East, and North Central Province to the rest of the national economy and improving opportunities for farmers and others in those areas to export their produce easily to other countries. Instead, we spent billions of borrowed money (at high interest rates) on an airport in the middle of nowhere, a cricket stadium that rarely gets used, conference halls, theatres, and countless other projects that have contributed little to nothing to the country’s economy.

With debt-financed projects bringing in no revenue, Sri Lanka had to borrow more and more to provide government services while also borrowing to pay off loans. For example, a recent study by Vérité Research found that 89.8% of the increase in debt stock between 2015 and 2019 was to pay interest on past debt.

Sri Lanka’s post-war economic boom lasted only three or so years mainly because the high growth at the time was a sugar rush created by debt-fuelled infrastructure spending. Ideally, we should have made our economy more competitive to facilitate foreign and local private sector-led growth.

1.2 Bad Fiscal Policy

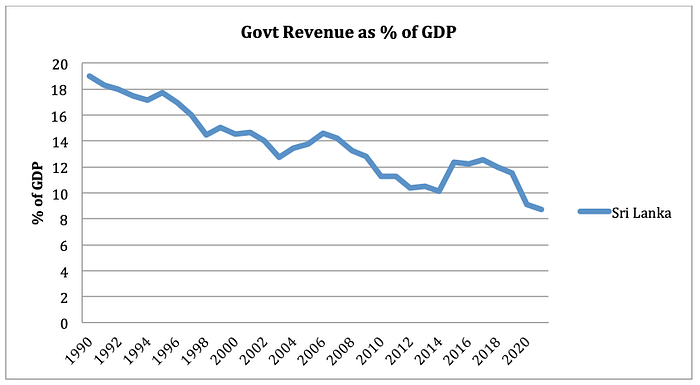

So why did we need to borrow so much? Simply put, the government’s tax revenue was inadequate to cover its costs. Therefore, it needed to borrow money. As shown in Figure 2, Sri Lanka’s government revenue declined steadily from around 18% in 1995 to around 10% in 2014. An ill-fated tax cut (to be discussed later) combined with less economic activity due to COVID-19 reduced revenues even further to 9.1% and 8.7% of GDP in 2020 and 2021, respectively. In order to finance growing fiscal deficits (government expenditure higher than government revenue), Sri Lankan governments relied on borrowing.

To make matters worse, our recent tax policies have burdened the poor significantly more than the rich. Instead of simplifying tax structures and focussing on a progressive tax system, officials reduced direct taxes (e.g. income tax and corporate tax), gave companies arbitrary tax holidays, and would increase indirect taxes such as VAT, import tariffs, and para-tariffs. This meant that in addition to being unfair, the over reliance on indirect taxes such as high import tariffs lead consumers faced with higher prices. At present, around 80% of the government’s tax revenue comes through indirect taxes.

Whilst our government revenue reduced, our expenditure increased, exacerbating the fiscal deficit even more. We already discussed the need to rationalise spending better. At the same time, the government continues to maintain a bloated and unproductive public sector. As of early 2020, in a country with a workforce of 8.5 million, estimates suggest that the public sector employs around 1.5 million people.

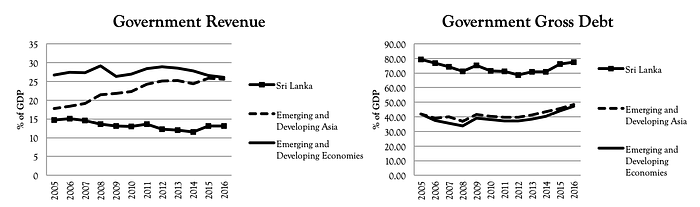

To put all of this in perspective, Sri Lanka has lower revenue and higher gross debt than other developing and emerging economies in Asia and the rest of the world (latest data from 2016).

1.3 Protectionism Leading to Export Revenue Loss

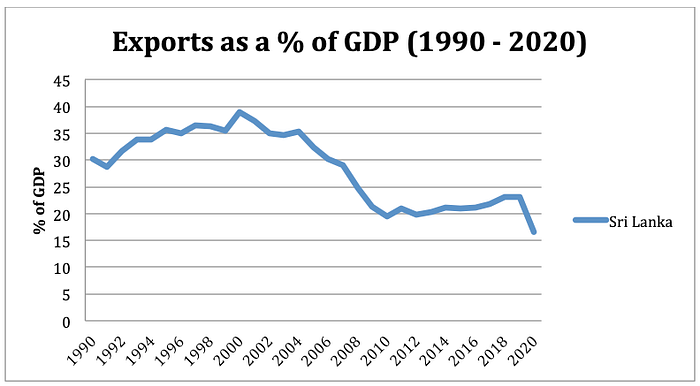

The negative impacts of both the above factors could be mitigated if a country had high levels of export revenue. Unfortunately, since the early 2000s, Sri Lanka pursued a toxic economic policy combination of low direct taxation, increased protectionism, and bridging the gap in finance through debt. As shown in Figure 4, revenue from exports (goods and services) as a percentage of GDP peaked in 2000 at 39% and reduced by almost half by 2015 (21%). The export sector saw a slight improvement between 2015 and 2019, but that increase was marginal and not even close to getting back to the peak. Of course in 2020 export revenues fell significantly due to the pandemic.

The fall in export revenue meant that less foreign currency was flowing into the country. The primary reason for the loss of export revenue is the continuous use of protectionism by successive governments to benefit the rent-seeking business elite. These businesses had established monopolies in the local market and did not want to compete against foreign competition. They also had no interest in innovating and bringing down their costs of production to compete in the export market. As a result, while consumers had to buy more expensive products due to protectionism, the economy was suffering as fewer and fewer export competitive industries emerged in the country.

It is no surprise that both times Sri Lanka attempted import-substituting industrialisation (1972–77 and 2019), the country has faced severe shortages and a foreign exchange crisis. Sri Lanka is a small-island economy and needs to import essential raw materials (e.g. oil, steel, aluminium, etc.). Therefore, no matter how much you restrict imports, you will always have a high import bill since even import substituting sectors have to use these raw materials. Notably, in pursuing import substitution, while we still spend on imports, the manufacturing sector is unable to garner export revenue since they are allocating resources towards inefficient import substituting industries instead of export competitive industries.

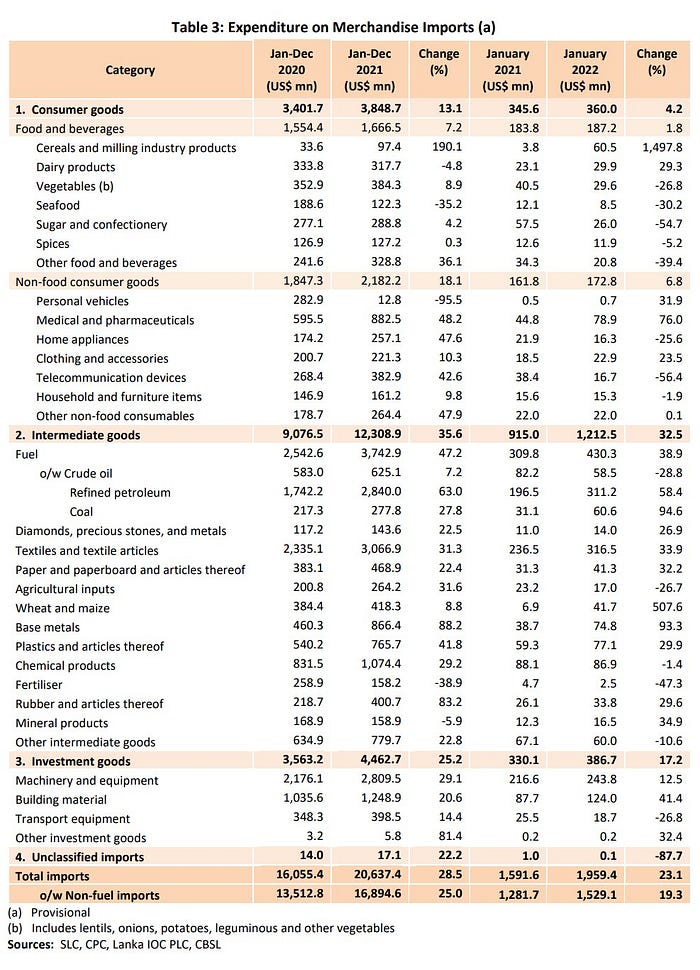

For example, as shown in Figure 5, only 20% of our total import cost is spent on consumer imports. Even amongst that, one-third is used for medicines, mobile phones, and laptops — consumer goods one would consider essentials in the modern economy. Meanwhile, 70% of the import cost is made up of raw materials (e.g. fuel) and intermediate goods (e.g. parts and components of machines).

Especially in the modern economy, where goods are produced through global supply chains, small economies like Sri Lanka have more opportunities to develop their export sector. This means that Sri Lanka no longer has to try and build an entire car and compete against Toyota. Instead, they can micro specialise in small parts and components (e.g. seat belt sensor) for Toyota cars. For this, they will have to import some intermediate products, add value by producing the sensor and then export it to another country to assemble the car. This is how countries like Malaysia and Vietnam developed their manufacturing sector in electronic goods. Unfortunately, Sri Lanka has been left behind in its economic policy evolution.

2. PUSH FACTORS

As is clearly evident above, Sri Lanka suffered from structural issues that placed the country in a sensitive position. Therefore, it was imperative that sound fiscal policy and economic management was necessary to ensure that the economy didn’t spiral out of control. However, a series of economic policies during the past few years exacerbated the country’s difficulties and when combined with the pandemic, led to the current crisis. Dr. W.A. Wijewardene and several others have written extensively about these policies, so I will only briefly touch on them.

2.1 Tax Cut in 2019

In November 2019, following the Presidential Election, the government embarked on a sweeping tax cut. The policy included reductions to income tax, corporate tax, and VAT, whilst also eliminating the PAYE (Pay As You Earn) system. This reduced government revenue by around 33% (approximately Rs. 600 billion per year). The fall in revenue led to multiple negative outcomes:

- Loss of revenue and the consequent increase in the fiscal deficit led to an increased need for further debt

- Credit rating agencies rightly assessed that the loss of revenue would make it harder for Sri Lanka to repay its existing and future debt, leading to a credit rating downgrade. The downgrade meant that the interest rates we paid for debt from international capital markets were significantly higher. In effect, following this downgrade, no one wanted to lend to Sri Lanka and the country’s access to development finance dried up.

2.2 Excessive Money Printing

As access to external financing instruments narrowed, the Central Bank embarked on a policy to print money to try and finance spending gaps. I won’t go into detail on this because anyone with a basic economics degree understands that excessive money printing leads to inflation. Yet, officials believed otherwise. The money printing obviously led to an increase in rupee circulation, and especially combined with COVID-19 induced lockdowns the money supply overwhelmed the economy, leading to high inflation. Some justified this policy as a “home grown” version of Modern Monetary Theory (MMT), but now even those who champion Modern Monetary Theory (MMT) have distanced themselves from the policy that was pursued in Sri Lanka.

2.3 Attempting to “Fix” the Exchange Rate

The slowdown of the export sector, credit ratings downgrades, and excessive money printing, all led to the gradual depreciation of the rupee. The Central Bank then decided to artificially fix the exchange rate at US$ 1 at around Rs. 200. This led to another series of negative outcomes:

- The country’s foreign reserves had to be used in order to keep the exchange rate at this artificially low level. Put simply: the Central Bank sold the dollars it had in reserve to increase demand for rupees.

- Due to extremely low exchange rate, Sri Lankan migrants abroad and exporters stopped bringing in money into Sri Lanka through official channels. Although informal channels such as the “Havala” system has existed for many decades, the significance of the gap between the formal exchange rate (e.g. $1 = Rs. 200) and the informal exchange rate (e.g. $1 = Rs. 280) meant that many migrants who have used the formal system were incentivised to switch to the informal system. Likewise, exporters would park their revenue overseas in order to circumvent subsequent policies that forcefully converted foreign exchange revenue into rupees. This was especially problematic since, as explained earlier, many exporters depend on importing their raw materials.

All this led to the rapid reduction in Sri Lanka’s foreign exchange reserves. At the end of 2019, Sri Lanka’s foreign reserves were approximately $8 billion (which could cover around 3–4 months of imports). In March 2022, foreign reserves were below $1 billion (which covers less than a month’s imports). On the 5th of May 2022, the Finance Minister announced that the country’s usable reserves are $50 million (which is equivalent to the cost of one shipment of fuel).

The fall in foreign reserves obviously meant that the country has found it difficult to import goods for manufacturing and shortages of essentials such as gas and fuel for many months now (due to a shortage of forex in the banking system).

After artificially fixing the exchange rate at such a low level for so long, the sudden decision to free-float the exchange rate instead of a managed float led to the rapid depreciation of the currency. Moreover, at the time, officials also failed to implement safeguards commonly used when floating an exchange rate such as the increase in interest rates to manage inflationary pressures.

2.4 Chemical Fertiliser Ban

In 2021, the government also decided to ban the importation of chemical fertiliser and failed to deliver on its promise to provide adequate stocks of organic fertiliser. Agricultural experts suggest that crop yield has dropped between 15–30%, while some even estimate the drop by as much as 40%. The agriculture sector accounts for more than 20% of the country’s workforce and the impact on crop yields had a direct impact on their livelihoods. Furthermore, the drop in crop yield required the government to spend already scarce foreign exchange to import rice. For example, in November 2021, the government imported $13 million worth of rice from Myanmar.

3. The Role of COVID-19 and the Russian Invasion of Ukraine

COVID-19 had a significant impact on Sri Lanka’s economy, most notably on the country’s tourism sector and briefly on its export sector as well (when foreign demand dried up during lockdowns in 2020). However, as discussed above, the current economic crisis was not caused by the pandemic. Instead, the pandemic accelerated the pace at which the country was heading towards the crisis. The economy was already set on a path towards a major crisis due to a series of bad policy choices. Similarly, the Russian-Ukraine situation exacerbated the crisis due to higher fuel prices and disruptions to Russian and Ukrainian tourist arrivals (a relatively large source of tourism since the pandemic).

Note: If time permits, I will share another explanatory note on the IMF process and debt restructuring